HAWT DAWG, we’re on a tear now!

Households increased debt during the third quarter at the fastest pace in 15 years due to hefty increases in credit card usage and mortgage balances, the Federal Reserve reported Tuesday.

Total debt jumped by $351 billion for the July-to-September period, the largest nominal quarterly increase since 2007, bringing the collective household IOU in the U.S. to a fresh record $16.5 trillion. That’s an increase of 2.2% from the previous quarter and 8.3% from a year ago.

…The credit card balance collectively rose more than 15% from the same period in 2021, the largest annual jump in more than 20 years, according to the New York Fed, which released the report. The increase “towers over the last eighteen years of data,” a group of Fed researchers said in a blog post on the central bank site.

Our lying eyes and bleeding bank accounts know who to blame, even though we also know we’re not supposed to blame them.

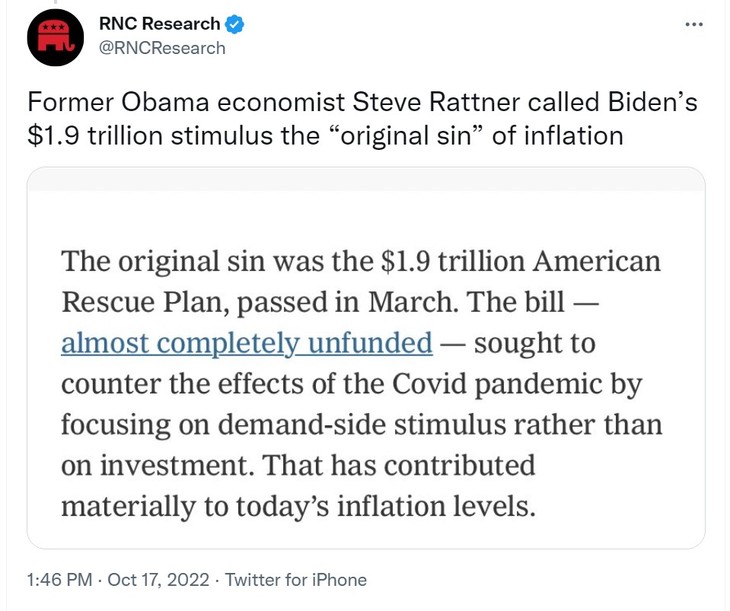

…During a press conference yesterday, Press Secretary Karine Jean-Pierre was asked about the start of inflation and accidentally made an admission. Jean-Pierre said what we’ve been saying all along.

REPORTER: "18 months ago when the president took office, inflation and gas prices starting rising."

KARINE JEAN-PIERRE: "18 months ago the president signed the American Rescue Plan" pic.twitter.com/fGi2Zzm2j5

— RNC Research (@RNCResearch) October 17, 2022

Derp. Even Obama’s economist was calling out the ludicrously named “Inflation Reduction Act” for producing the exact opposite effect.

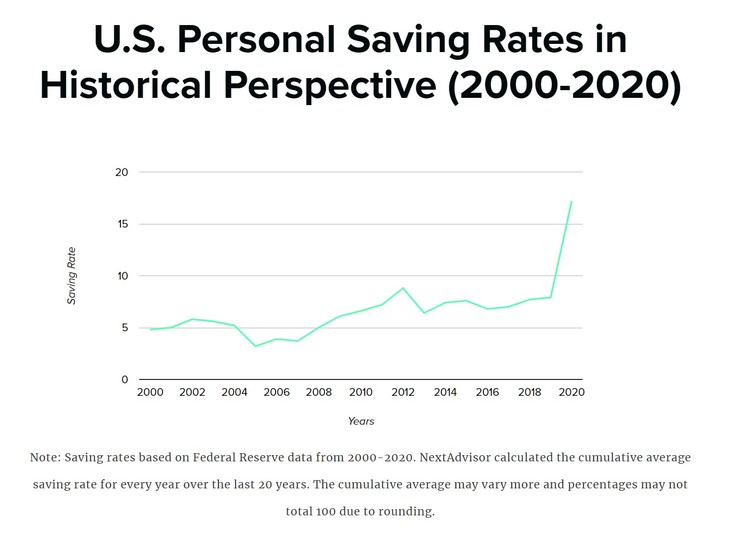

And now those inflationary jumps have had time to begin taking their toll on Americans’ savings. Mortgage rates and inflated housing prices are a huge part of that overall increased debt load, moving up $1T to almost $12T on the books today. Credit card balances now account for $930B. Correspondingly, the personal savings rate has fallen from its all-time high in 2020…

…The U.S. personal saving rate — the percentage of people’s income remaining each month after taxes and spending — skyrocketed to a record 32.2% in April, up from 12.7% in March, according to the U.S. Bureau of Economic Analysis. At the same time, consumer spending fell 12.6% as the economy slowed down and unemployment rose.

Data from the Federal Reserve Bank of St. Louis shows the previous record American saving rate was 17.3% in May 1975, at the tail end of a recession spurred by rocketing gas prices, government spending on the Vietnam War, and a Wall Street stock crash. Over the last 10 years, it has hovered in the 6-8% range.

…to now hovering in the low to mid 3% range. There is no longer “excess” at the end of the month available for average folks to tuck away. There is always a certain percentage of Americans who live paycheck to paycheck, but under Biden’s inflation-driven economy, that number has risen to 2/3s of households in the U.S.. While they are still employed, that same amount of money is worth so much less – in fact, if you felt like you were losing ground? You were right.

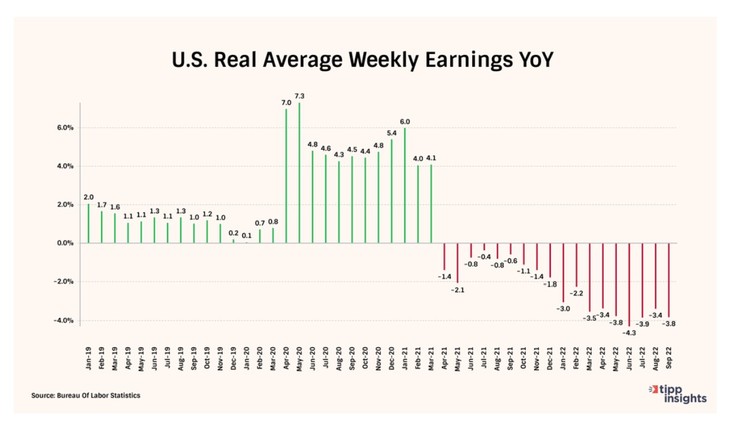

…Real income, also known as real wage, is the amount of money earned after adjusting for inflation. Real income is distinct from nominal income, which does not include such adjustments.

Wages are stagnant. U.S. real average weekly earnings, measured year-over-year, have been in the negative territory for eighteen months.

That’s a gruesome chart. There’s also no rainy day fund money set aside – or if there was, it’s already been eaten through – so those life emergencies are going on credit cards as well, at an average interest rate of 16.9% (Cha-CHING for MBNA’s favorite senator from Delaware!). Whatever household progress was made over the past couple years of plenty in getting financially stable has, in many instances, been nearly wiped away, leaving citizens in precarious positions. And if you’re laid off, man. Terrifying as things slow down. There are still plenty of opportunities out there for people who want to work, as in WORK. That may be the thing that saves folks.

Hardly comforting are the malignant economic neophytes running the cheering section from the White House. They don’t have a damn clue. CPI comes in at 7.1%?

“Today’s report shows that we are making progress on bringing inflation down, without giving up all of the progress we have made on economic growth and job creation. My economic plan is showing results, and the American people can see that we are facing global economic challenges from a position of strength.”

CLOWNS.

CNBC, another praetorian mouthpiece for the regime, quoted the N.Y. Federal Reserve as it tried to gussy up the news by crediting “robust consumption.” YEAH. Nice way to phrase EVERYTHING COSTS A BUTTLOAD MORE. That was among other bad news they plopped in the middle of the statement. Check out how they put it:

…New York Fed researchers attributed the credit card growth to “very robust” consumption, rising prices and consumers using substantial levels of savings that remain on accounts.

I translate that as consumers have “reached the end of available resources due to runaway costs in all aspects of all markets.” Household pockets are dang near turned inside out and wrung dry.

But? Robustly!

CLOWNS,

Join the conversation as a VIP Member