The saga of FTX founder Sam Bankman-Fried gets more bizarre and more disturbing, as competing narratives begin to clash.

Bankman-Fried rose to prominence as the Democrats’ second-largest campaign donor after George Soros over the past couple of years, as well as the darling of the glitterati who always are taken in by hucksters who promote virtue signaling over basic reality. He was a huge donor to Joe Biden’s campaign in 2020, and continued his giving spree in 2022 through major campaign contributions both to candidates and dark money Super PACs.

Ken Griffin, CEO of Citadel, highlighting one of the darkest details of the entire FTX situation.

How deep does the rabbit hole go?

What was FTX? pic.twitter.com/2tSSH0SCK2

— Luke Martin (@VentureCoinist) November 15, 2022

In return he got plenty of access to both politicians and regulators, and the kind of glowing media coverage that money normally can’t buy, but money given to Leftist causes usually can.

Bankman-Fried, it unsurprisingly turns out, is a fraudster. All that money that went into his pockets and those of the Democrats was obtained through fraud, yet nobody bothered to look because all the right people did very well out of the deal.

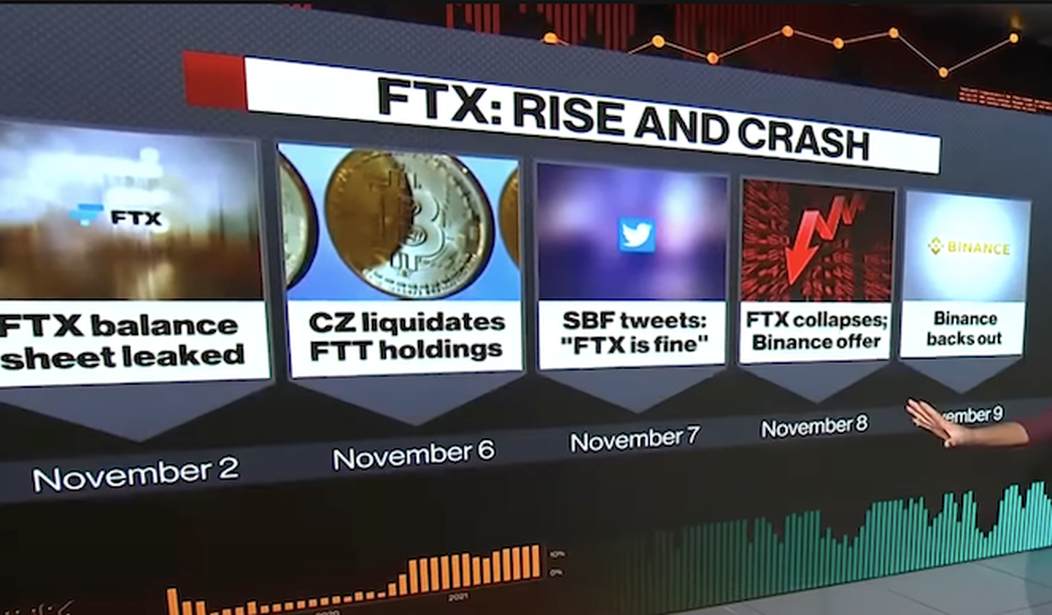

And, as always seems to be the case, the Left-benefiting fraud only came out once the Left benefited mightily–those campaign funds had already been spent by election day–which happens to be when the house of cards that Bankman-Fried began to collapse. It was a day after the election that the news of the collapse began to filter out, and the days after the election that the details of the fraud have begun to spread.

How convenient.

“The Next Warren Buffett.” That’s how Fortune magazine dubbed Sam Bankman-Fried, the crypto wunderkind who wore shorts, schlubby socks, and sneakers on stage with Bill Clinton and Tony Blair. But Bankman-Fried, worth an estimated $32 billion at his height, wouldn’t just be a financial oracle like Buffett. He would also be the second-coming of George Soros: By the end of this midterm election cycle, he’d become the second largest donor to the Democratic Party.

Before this week almost nobody outside the worlds of politics and finance had heard of the kid, but inside those worlds he was a power broker. Promising to spend a billion dollars to help the Left in the 2024 elections will do that for you. Whatever misgivings people may have had, they suppressed them in the pursuit of campaign cash.

As FTX took off with the pandemic-driven crypto boom, so did a carefully cultivated Cult of SBF. Only two years after FTX’s founding, the company purchased naming rights to the NBA’s Miami Heat stadium in a 19-year commitment of $135 million. Deals soon followed for college stadiums. A Mercedes Formula 1 team. National Baseball League umpire patches. Partnerships with Tom Brady and Gisele Bundchen.

In short order, profiles of the boy genius appeared everywhere. As cryptocurrencies soared in market value, SBF became the poster child for the libertarian ethos that crypto profits accrued to those most capable. He seemed to have access to the glitterati previously reserved for those with established connections within the intellectual elite.

The story of Bankman-Fried would seem to be one reminding us of the dangers of politicians and regulators being blinded by the lure of easy money, but The New York Times–easily one of the most effective propagandists for the Democrat Party–wants to assure us that things aren’t so simple. Bankman-Fried, we learn, isn’t that bad a guy and the politicians who vacuumed up the cash are largely blameless for being lured into his orbit.

The new article in the New York Times by David Yaffe-Bellany lays out the facts in ways that are clearly beneficial to SBF’s version of the story and leaves many of his highly questionable assertions without proper context or even the most minimal amount of pushback. The result isn’t to illuminate the shadowy world of crypto. It reads like if the Times had conducted an interview with Bernie Madoff after his ponzi scheme collapsed and ultimately suggested he just made some bad investments.

As one example, take a paragraph near the beginning of the article that quotes SBF’s dealings with hedge fund Alameda Research, the sister organization of FTX, run by SBF’s sometime romantic partner Caroline Ellison. The paragraph, one of just a few about Alameda, brushes past all the most important facts that have been reported by outlets like Reuters, Bloomberg News, and the Financial Times.

From the New York Times:

Alameda had accumulated a large “margin position” on FTX, essentially meaning it had borrowed funds from the exchange, Mr. Bankman-Fried said. “It was substantially larger than I had thought it was,” he said. “And in fact the downside risk was very significant.” He said the size of the position was in the billions of dollars but declined to provide further details.

SBF’s quote about “borrowing” billions between FTX and Alameda seems to be a wild mischaracterization, if we’re to believe reliable reporting by numerous other outlets, and paints the corporate three-card-Monte as some kind of innocent investment move gone wrong. At least $4 billion of FTX funds, including customer deposits, were moved to prop up Alameda, according to Reuters, and that’s just something you can’t do legally.

Stealing client funds–and that is exactly what Bankman-Fried did, was not just a poor investment decision made by a well-meaning investor who got into a bad trade. It was massive fraud. And it is much worse than that, because the “investment” made with those funds was in a fraudulant asset created out of thin air by the company itself. It created a crypto currency, declared it had value X, and then used that fake value to claim assets it never had.

It even paid employees and vendors with this worthless asset, while pocketing real assets and distributing them to politicians and other idiots who were happy to take the cash. Clients were left with little or nothing while others–not just Bankman-Fried but the people who enabled his scam–able to spend the client’s money as their own.

FTX held just $900 million in liquid assets, and its largest single asset was a cryptocurrency called Serum, according to the Financial Times. FTX held $2.2 billion worth of Serum, but the market value of all Serum everywhere was just $88 million. And you’re never going to guess who created Serum. Much like FTT, Serum was created by FTX and Alameda, according to Bloomberg News. The people behind FTX created their own fake money and they were treating it as though it was real dollars and cents.

But every single explanation in the new Times piece gives both SBF and cryptocurrency more broadly the benefit of the doubt, using the former billionaire’s quotes extensively, and even trying to position his attitude as one of self-reflection rather than ruthless calculation to make himself sound better.

Another excerpt from the Times:

Mr. Bankman-Fried did, however, agree with critics in the crypto community who said he had expanded his business interests too quickly across a wide swath of the industry. He said his other commitments had led him to miss signs that FTX was running into trouble.

“Had I been a bit more concentrated on what I was doing, I would have been able to be more thorough,” he said. “That would have allowed me to catch what was going on on the risk side.”

Did SBF “expanded his business interests too quickly” in some way? Did SBF just not “catch what was going on” with the risks he was taking? Or was the entire venture rotten to its core?

Paragraph after paragraph in the Times gives a gentle light to FTX’s extraordinary implosion, explaining that SBF’s “ambitions exceeded his grasp” or speculating that perhaps he was “overly dependent” on a small group of advisors.

The New York Times isn’t filled with naifs unable to understand the intricacies of a massive fraud. Sam Bankman-Fried isn’t pulling one over on them.

They are instead covering for the fraud, making it sound innocent, because vast numbers of very powerful people benefited from the fraud and it is they, not Bankman-Fried, who need the cover that a puff piece on this scumbag can provide.

NEW: @SenGillibrand is donating the campaign money she received from @SBF_FTX (Sam Bankman-Fried).

Her campaign & joint fundraising committee received a $16,600 this year from the former @FTX_Official CEO.

She's also a co-sponsor of a crypto bill.https://t.co/rBhY6KI1Y9— Brian Schwartz (@schwartzbCNBC) November 15, 2022

None of these powerful people is being hurt in any appreciable way by the collapse of FTX. Rumors that Tom Brady lost his shirt are ridiculous. Nobody that smart and savvy puts his entire net worth into a shady 3 year old Ponzi scheme. That requires decades of fraudulant activity that a Bernie Madoff can pull off, not a kid in shorts and tennis shoes.

This plays like a SBF parody video.

pic.twitter.com/I3VzzCig5s— Chip – onthechain.io (@stephenchip) November 12, 2022

But all those Leftist politicians sure benefited from the scheme, and outlets like the Times are going to do their best to cover for them. Allowing the scheme to collapse two years out from the next election will minimize the damage, and it will be a non-issue by then. Just as the Hunter Biden laptop will be. Old news.

This is how the Establishment™ does its dirty business. Billions of dollars from normal people disappear, but at least the Democrats got their dough. The elections worked out for them, so no biggie.

Join the conversation as a VIP Member