“Financial distress.” There’s a phrase we’re not supposed to be familiar with in these halcyon #Bidenomics days of milk and plenty of honey…and yet we are.

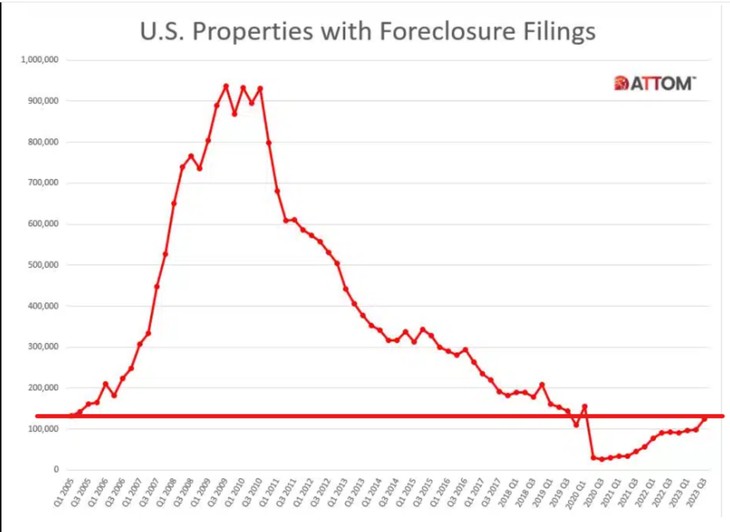

Home foreclosure activity in the US surged to the highest level since the start of the pandemic, a sign that the financial aftermath of COVID-19 has been wearing out cash-strapped homeowners.

Foreclosure filings – including default notices, scheduled auctions, and bank repossessions – jumped 28% in the third quarter from the prior quarter to 124,539, the real estate data group ATTOM said in a recent report. That represents a 34% surge from a year ago, attesting to growing financial distress among US homeowners.

And foreclosure activity appears to have been increasing steadily through 2023. September alone saw an 11% jump in foreclosure filings to 37,679, up 18% from September of last year, researchers added.

Mortgage lenders, meanwhile, began the foreclosure process on 68,961 properties in the US over the past quarter, up 3% from the third quarter of 2022.

Part of this uptick can be attributed to the same shock that those who are actually going to have to repay student loans are facing. There have still been some been COVID-era mortgage forebearance and foreclosure moratorium programs in effect that have only recently expired or are due to shortly. So some of these properties were already in trouble even before the first pandemic mortgage relief programs began under Trump. This merely put the pain off for them for a while.

For some in trouble, the break might have given them a chance to get their act together financially and refinance while rates were still low, but that opportunity is no longer an option. Rising mortgage rates, besides squelching re financing for those in a bind, are also putting a damper on them unloading their property to get out from under the burden entirely.

Buyers have gone missing, and people are staying in their homes rather than move up to a place a little chi-chier.

Existing-home sales data for September, set for release this week, is expected to show that sales slumped to the lowest level in more than a decade as mortgage rates rose. More bad news could be around the corner.

Rising rates have weighed on everything from housing market sentiment to mortgage applications in recent weeks. Mortgage rates measured by Freddie Mac‘s weekly gauge quickly rose past 2022’s high of 7.08% in mid-August—and largely kept climbing. The average mortgage rate last week was 7.57%, Freddie Mac said, the highest since late 2000.

Analysts say the full brunt of the rates has yet to be felt because of the lag between contract and closing time, so August’s figures are still reflecting summer sales data. The sad-enough picture we have now could be much worse in the next report, which will be September’s numbers.

…That’s likely to change with the release of September’s report, expected on Thursday. Economists polled by FactSet expect existing-home sales to drop 3.5% to the lowest level since October 2010. Should the expectations come to pass, it will be the greatest month-over-month decline since November 2022, when rising rates similarly snuffed out buying activity.

I mean, this is a gruesome headline:

Mortgage rate races toward 8% after hitting a high not seen since late 2000

Mortgage rates are corelated to long term rates.. Good luck finding a rate less than 8% on a conventional loan now. pic.twitter.com/AXuITC19Wu

— Frog Capital (@FrogNews) October 17, 2023

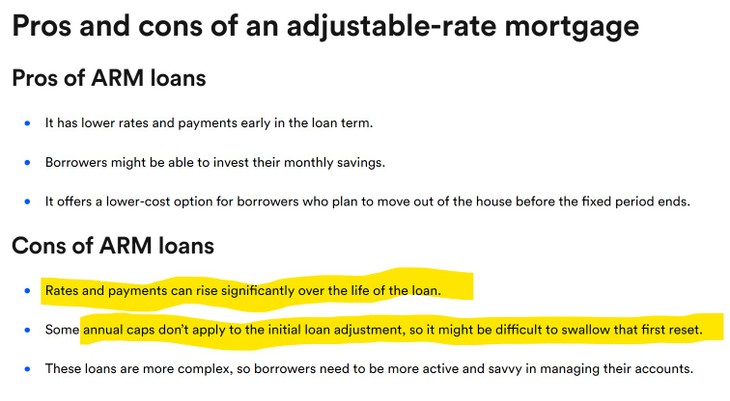

If you have an adjustable rate mortgage, you have to be sweating bullets. Unsurpriingly, they weren’t very popular – or necessary – when rates were rock botteom, even for less than stellar credit, but now?

They’re becoming more popular but come with their own set of “buyer beware” cautions.

Most of the news on this clings to the “stable economy” and job market line that has the Biden administration moaning about our “disconnect” from their magnificent economy. How can the peasants be so gloomy?

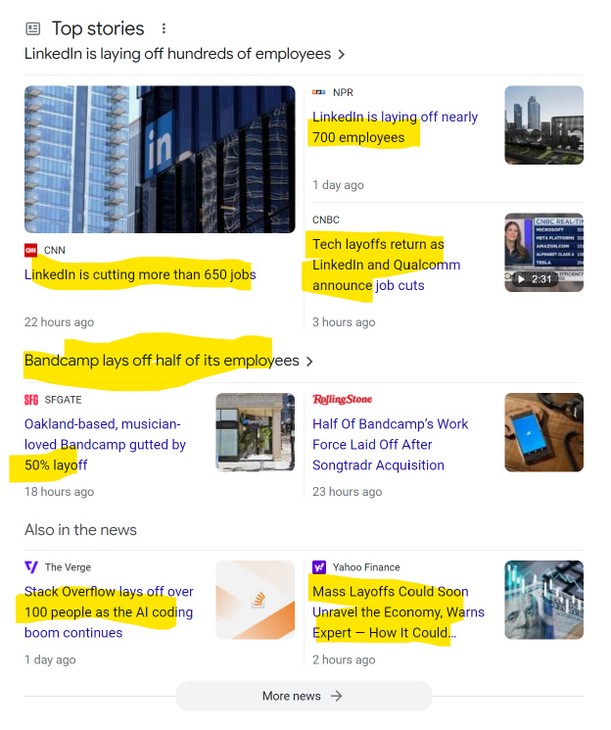

As for that rock-solid job market POTATUS’ master manipulators keep telling us we have (because no one in his right mind has any faith in the BLS numbers), a quick Google news check isn’t showing anything rock solid.

In fact, analysts are kind of worried about the job market crashing along with everything else.

Mass Layoffs Could Soon Unravel the Economy, Warns Expert — How It Could Impact Your Investments

…But a string of layoffs at large companies this year has raised fears that jobless claims will soon move higher — and stocks and other investments could take a hit because of it.

On Monday, LinkedIn became the latest high-profile employer to announce layoffs when it said it would cut about 668 jobs, or roughly 3% of its workforce, The New York Times reported. That news followed an earlier announcement of 716 LinkedIn layoffs in May.

Among the other large employers to announce hundreds or thousands of layoffs in 2023 include CVS, T-Mobile, Qualtrics, General Motors, Cisco and Alphabet, according to talent search company Mondo.

At least one leading economist — Torsten Slok of Apollo Global Management – worries that mass layoffs will soon be reflected in key economic data that could negatively impact investor portfolios, MarketWatch reported.

Are they disconnected, too? Or do they shop at the same supermarket I do?

It’s also hard to pay the mortgage when your union goes out on strike or your tech company downsizes.

For interest’s sake, the real trouble areas at the moment aren’t really that surprising as they are also very expensive places to live.

…Metros that posted the greatest number of foreclosure starts in the third quarter included New York (4,514 foreclosure starts); Chicago (2,584 foreclosure starts); Houston (2,279 foreclosure starts); Los Angeles (2,273 foreclosure starts); and Philadelphia (2,104 foreclosure starts).

States with the highest foreclosure rates included New Jersey (one in every 595 housing units with a foreclosure filing); South Carolina (one in every 730); Delaware (one in every 739); Nevada (one in every 763); and Maryland (one in every 780).

When those houses go under, so does the tax base, particularly when it’s too expensive to purchase that distressed property or there are no jobs available for a buyer who might want to.

Bets are increasing that the Fed will cut rates in 2024, but that’s throwing the bones wishful. Even if they did, this little train of dominoes they’ve already set to tilting may be on its way and unstoppable.

And their “soft landing” dreams are going to need a crash pillow.

Join the conversation as a VIP Member