Yup. We sure are humming right along, aren’t we?

Let’s raise a toast to all that good news.

I mean, when even the money gurus can’t get out of their own way, there’s something going on.

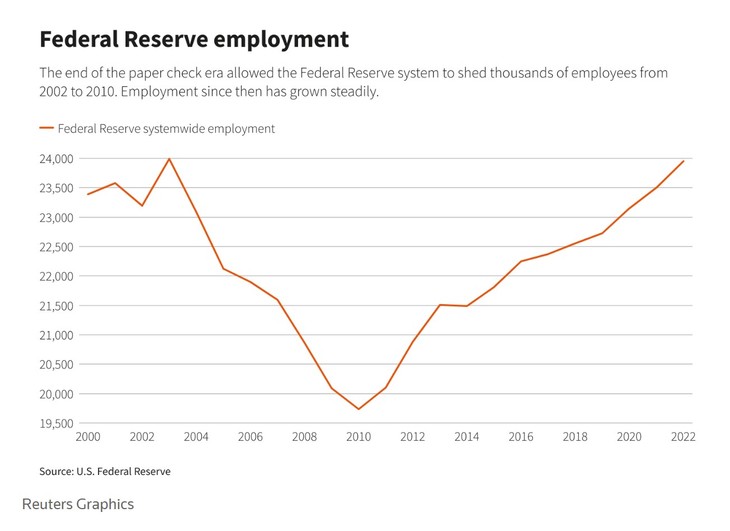

The U.S. Federal Reserve system is cutting about 300 people from its payroll this year, a small but rare reduction in headcount across an organization that has grown steadily since 2010 as its reach in the economy and regulatory agenda have expanded.

A Fed spokesperson said the cuts are focused on the staff of the U.S. central bank’s 12 regional reserve banks and mainly hit information technology jobs, including some no longer needed because of the spread of cloud-based computer software, and positions connected to the Fed’s various systems for processing payments, which are being consolidated.

The spokesperson, who would not speak for direct attribution, said the staff cuts represented a combination of attrition, including retirements, and layoffs.

…While small compared to the size of the Fed, it is the first time budgeted headcount has fallen since 2010.

Then again, if you look at a chart of the growth of the Fed over the past almost 14 years…there’s something going on there, too, and not necessarily a good thing.

These cutbacks are mostly tech jobs according to the announced plans, so “learn to code” advice isn’t going to be appropriate. It truly hasn’t been for the bulk of the announced lay-offs so far, as the tech sector’s taken solid hits between last fall’s Silicon Valley bloodbaths and what looks to be coming now. Tech lay-offs have been announced this month at start-up AirTable (rocky going there), along with more at Cisco, Roku, and Google to name a few.

Industries across the board are paring back.

The RTO (return to office) movement is also having an effect on employment numbers, and some analysts believe that’s by design. This doesn’t require notifications or compensation pay-outs, because an employee basically quits if they don’t comply.

The return-to-office debate sees no end in sight as companies grapple with mandates and the employee backlash that follows.

While a whopping 90% of companies plan to implement return-to-office policies by the end of 2024, flexibility remains a top priority for employees — and the lack of it might push them to seek other opportunities.

However, that is exactly what some companies want, according to workplace experts that CNBC Make It spoke to.

…“A company might use a return to office mandate as an opportunity to restructure its workforce.”

Schawbel added that one company that could be employing this “covert layoff” tactic is AT&T, which recently mandated that 26,000 managers across 50 states work in person — but only at offices in just nine locations.

The billionaire property developer speaking in the short video below about returning the balance to where an employee knows they’re lucky to have a job was forced to eat his words and crawl down for an apology afterward.

This is truly incredible.

Billionaire property developer Tim Gurner said that "We need to see unemployment rise. We need it to rise 40-50%. We need to see pain in the economy. We need to remind people that they work for the employer, not the other way around." pic.twitter.com/E86B8qnn31

— unusual_whales (@unusual_whales) September 16, 2023

A large part of the outrage at his little pearl of wisdom was that fact that the world he described – the employer/employee relationship – doesn’t exist any more in the traditional sense. It’s been proportionally blown out of the water. In some industries – admittedly not all – the executive to employee pay imbalance is in Louis XIV territory, and the peasants are actively rattling the cage doors for their slice of cake.

For instance, while the UAW demands seem insane, greedy, and self-defeating on their face, when you look at them in relation to what they’re paying, say, the insipid head of GM (Her 2022 compensation comes in at a paltry $28,979,570 which, if you can believe it, meant she made a little less than in 2021.)? You have a sense of where the anger may be coming from.

…Gurner admitted his remarks “were wrong” in a subsequent apology.

In the U.S. from 1978 to 2021, according to the Economic Policy Institute, economic productivity grew more than 60%. Yet the typical worker’s wages — which in previous decades had roughly tracked productivity — grew just 18%. The wages of the top 1% of earners, however, grew 385%. CEO pay grew by more than 1,000%.

Who blinks first, and who is willing to compromise in good faith to keep a company afloat comes into play, knowing full well that recent history shows that as little employee loyalty as there is, there is even less from the company for employees. It’s a toxic atmosphere, compounded by the realities in a worsening overall fiscal situation from consumer to company head to the halls of Congress.

Where the disconnect between dreams and difficulties lies now is the weakening economy. If there ever was a time NOT to demand the moon in hostile labor negotiations, now is probably it. UPS drivers might well have a sweet deal on top of well-deserved air-conditioning, but if shipping falls off a cliff with the consumer’s purchasing power, so do those brown trucks.

Bidenomics is running on empty. Coincidentally, so is the Federal reserve.

…The staff reductions are happening at a sensitive time for the Fed. It has booked $100 billion in losses in recent months on operations that currently involve paying more in interest to banks on reserve deposits at the Fed than the central bank earns from its roughly $7.5 trillion portfolio of bonds and mortgage-backed securities.

Unlike federal agencies that spend tax dollars allocated by Congress, the Fed is self-funding. Its earnings from its asset holdings and fees charged to banks for a range of services are used to pay the roughly $6.3 billion in annual expenses of a system that employs nearly 24,000 people in Washington and other cities across the country.

In most years the Fed generates a profit that is turned over to the U.S. Treasury. But since the central bank began to increase interest rates to control a surge in inflation, it has been spending more than it earns each year, and in effect gives the Treasury an IOU to be paid later.

Bidenomics in a nutshell in that last sentence:

I’LL GLADLY PAY YOU TUESDAY FOR A DOUBLE CHEESEBURGER WITH FRIES, APPLE PIE AND A SHAKE TODAY

~ Joe Wellington Wimpy Biden

Join the conversation as a VIP Member