“Here at home, inflation is coming down,” Joe Biden declared exactly one week ago. “Inflation has fallen every month for the last six months,” he continued, “while take-home pay has gone up.”

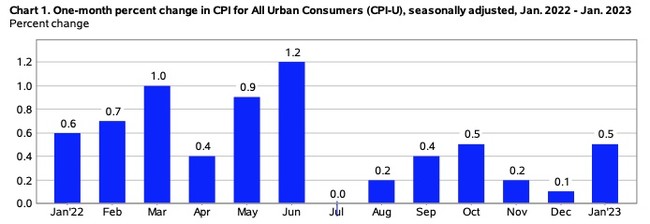

A week later, the consumer price index shows a 0.5% increase in January, with year-on-year inflation up to 6.4%. And let’s not forget that these measures compound on earlier high-inflation reports, too:

The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.5 percent in January on a seasonally adjusted basis, after increasing 0.1 percent in December, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 6.4 percent before seasonal adjustment.

The index for shelter was by far the largest contributor to the monthly all items increase, accounting for nearly half of the monthly all items increase, with the indexes for food, gasoline, and natural gas also contributing. The food index increased 0.5 percent over the month with the food at home index rising 0.4 percent. The energy index increased 2.0 percent over the month as all major energy component indexes rose over the month.

The index for all items less food and energy rose 0.4 percent in January. Categories which increased in January include the shelter, motor vehicle insurance, recreation, apparel, and household furnishings and operations indexes. The indexes for used cars and trucks, medical care, and airline fares were among those that decreased over the month.

How many times has Joe Biden declared victory over inflation now? Three? Four? Double digits? This chart in the BLS report shows once again that inflation has not ended as a threat, not even with gas prices moderating over the last couple of months again:

The rate of inflation in January is the highest since October and tied for the highest since June. Inflation has not ended, and given the compounding nature of inflation, it may not even be slowing up that much.

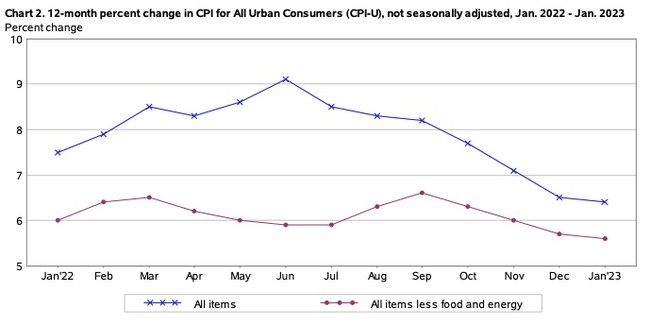

The White House will hope to elide that point by focusing on this BLS chart:

It’s true that year-on-year CPI inflation (and other measures) have drifted downward from last summer. However, last summer’s measures were compared to the summer of 2021, when inflation had really just started to slowly move up. The January 2023 reading compares to the January 2022 measure, when inflation went up 7.5% and hit a new high. In other words, this month’s CPI reading shows that inflation went up 6.4% on top of the 7.5% increase a year ago over January 2021, when Biden took office. And this is hardly the only month where compounding has been or will be taking place:

U.S. inflation:

Jan 2021: 1.4%

Feb 1.7%

Mar 2.6%

April 4.2%

May 5.0%

June 5.4%

July 5.4%

Aug 5.3%

Sept 5.4%

Oct 6.2%

Nov 6.8%

Dec 7.0%

Jan. 2022: 7.5%

Feb 7.9%

Mar 8.5%

April 8.3%

May 8.6%

June 9.1%

July 8.5%

Aug 8.3%

Sept 8.2%

Oct 7.7%

Nov 7.1%

Dec 6.5%

Jan 2023: 6.4%— Lucas Tomlinson (@LucasFoxNews) February 14, 2023

That’s the reason those year-on-year numbers are sloping down. It’s not that inflation is moderating; it’s that inflation is compounding. We are stuck in an inflation rut.

And even this report underestimates the impact this compounding inflation has on American households. Washington Post econ reporter Heather Long pulls out the key data in the tables:

It's not hard to understand why Americans are still frustrated w/this economy when you look at the latest inflation report:

Groceries +11.3% in past yr

Eating out +8.2%

Natural gas +26.7%

Electricity +11.9%

Rent +8.6%

Airfare +25.6%

Vehicle insurance +14.7%

Pet services +8.4%— Heather Long (@byHeatherLong) February 14, 2023

And let’s not forget the impact that this inflation has on wages, as Jeff Cox reminds CNBC readers:

Rising shelter costs accounted for about half the monthly increase, the Bureau of Labor Statistics said in the report. The component accounts for more than one-third of the index and rose 0.7% on the month and was up 7.9% from a year ago.

Energy also was a significant contributor, up 2% and 8.7% respectively, while food costs rose 0.5% and 10.1% respectively.

Rising prices meant a loss in real pay for workers. Average hourly earnings fell 0.2% for the month and were down 1.8% from a year ago, according to a separate BLS report.

So once again, buying power erodes while Biden brags about nominal wage increases. It’s tough to be more out of touch than that.

A look at the broader categories in Table A shows little sign of moderation. Prices dropped month-on-month in only three categories: fuel oil, used cars, and medical care services. Of those, only used cars showed a year-on-year decline. Every other category went up by at least 0.4% except non-food commodities (0.1%) and new vehicles (0.2%). This wasn’t a case of an enormous spike in one or two areas creating an inflation artifact out of an otherwise moderating economic environment. This is broad-based inflation that shows no sign of moderating at all.

Gas prices did go up 2.4% in January, so expect the White House to dust off its “corporate greed” argument about the oil companies and gas station owners. However, gas prices fell 7.0% month-on-month in December and are only up 1.5% year-on-year in this report. Electricity is becoming far more of a problem in inflation, likely thanks to the combination of supply restrictions on coal and natural gas combined with pressure to move to electric vehicles and electric home appliances. Electricity is up 11.9% YoY, 0.5% MoM, and we can expect that inflation to get worse in the spring and summer months when the weather warms up again.

What will the Federal Reserve do? They use the personal consumption expenditures index as their gauge of inflation, and try to match it up to the prime interest rate. That usually stops inflation, or at least it does theoretically, but it’s been a long time since that theory has had to be tested. We’ll get the January PCE Index reading at the end of the month, but that has been declining for the last few months. If that starts ticking back up again — and this report seems to clearly indicate it will — expect Jerome Powell to accelerate the rate of interest hikes again to kill demand. In the absence of real supply-side policies from the White House and Congress, demand destruction is the only tool in the bag for Powell, even though it will likely trigger a recession at some point.

Join the conversation as a VIP Member