It could be better, but the producer-price index results for October could have been worse, too. Today’s report from the Bureau of Labor Statistics puts the annual PPI inflation rate at 8%, its lowest level in more than a year, even if it’s still too high. Even better, the monthly rate of increase only hit 0.2% — although that’s mainly due to a significant decrease in service prices:

The Producer Price Index for final demand increased 0.2 percent in October, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices rose 0.2 percent in September and were unchanged in August. (See table A.) On an unadjusted basis, the index for final demand advanced 8.0 percent for the 12 months ended in October.

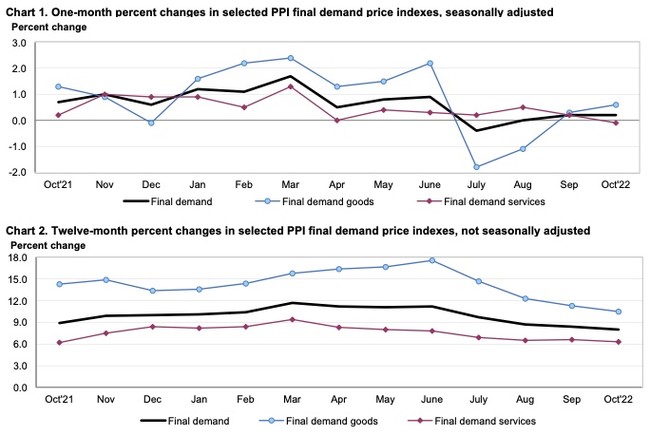

In October, the rise in the index for final demand can be attributed to a 0.6-percent advance in prices for final demand goods. In contrast, the index for final demand services decreased 0.1 percent.

Prices for final demand less foods, energy, and trade services advanced 0.2 percent in October following a 0.3-percent rise in September. For the 12 months ended in October, the index for final demand less foods, energy, and trade services increased 5.4 percent.

Let’s look at these results in the context of performance over the past year:

Not terrible, but still not good. PPI inflation in services has declined, especially in month-on-month reports, but service-related PPI didn’t drive the numbers over the past year either. PPI inflation on final-demand goods did, and that’s rising again after three months of declines and stasis. A rate of 0.6% inflation in October does not look like a great signal for what will follow in the next few months, even if it’s not nearly as bad as the first six months of this year.

It’s still the lowest annual PPI inflation rate in a year or more, though, following September’s 8.4%, which was itself a year-long-or-more low in the PPI. That may well signal a moderating trend in inflation, one which may speak to Federal Reserve officials looking to trim the sails of its interventions against inflation. The problem is that the effects of this moderation are scattershot and may not make its way to consumer mindsets.

For instance, look at where prices fell and prices rose month-on-month in this report, in overall categories:

- Final demand foods, all: 0.5%

- Final demand energy: 2.7%

- Nondurable consumer goods: 0.3%

- Durable consumer goods: -0.1%

And more granularly:

- Fresh fruit: 11.5%

- Vegetables: 22.4%

- Eggs: 15.0%

- Processed chickens: -12.5%

- Processed turkeys: 1.9%

- Gasoline: 5.7%

- Home heating oil: 9.4%

These are mainly excluded from “core” PPI, but these are the goods that consumers rely on most heavily. If these are still going up this dramatically, then the overall PPI inflation decline isn’t going to reach them.

This did beat expectations and sparked a small rally on Wall Street, as Jeff Cox reports for CNBC:

Wholesale prices increased less than expected in October, adding to hopes that inflation is on the wane, the Bureau of Labor Statistics reported Tuesday.

The produce price index, a measure of the prices that companies get for finished goods in the marketplace, rose 0.2% for the month, against the Dow Jones estimates for a 0.4% increase. …

On a year-over-year basis, PPI rose 8% compared to an 8.4% increase in September and off the all-time peak of 11.7% hit in March. The monthly increase equaled September’s gain of 0.2%.

Excluding food, energy and trade services, the index also rose 0.2% on the month and 5.4% on the year. Excluding just food and energy, the index was flat on the month and up 6.7% on the year.

One significant contributor to the slowdown in inflation was a 0.1% decline in the services component of the index. That marked the first outright decline in that measure since November 2020. Final demand prices for goods rose 0.6%, the biggest gain since June [and] traceable primarily to the rebound in energy, which saw a 5.7% jump in gasoline.

If this signals a moderating trend, great. However, the fact that fuel prices are rebounding again suggests that distribution chain costs will continue to rise, and with it consumer prices and overall inflation — especially where it matters most to consumers. Don’t break out the bubbly … which costs 0.7% more in October than it did in September, too.

Join the conversation as a VIP Member