Normally, we’re talking about San Francisco’s spectacular commercial real estate troubles on top of everything else wrong with that city. But today I came across something concerning another city that was kind of surprising – I don’t know, maybe I shouldn’t have been. It is bluer than blue, but I never think of Atlanta as a potential problem.

It turns out, they are really worried about their downtown.

Atlanta has been one of the Sunbelt’s biggest boomtowns, where the population and job market are growing fast. But you would never know that from its slumping office market.

Vacancy rates are soaring and companies are competing to unload space in the sublease market. Office values and rents are falling. Developers are delaying new office projects, while office defaults are mounting.

Atlanta’s commercial-property turmoil shows that even Sunbelt cities with thriving economies can’t escape the office-sector meltdown. Strong job growth hasn’t made up for the city’s anemic return-to-office rate, a glut of new office supply in the years leading up to the pandemic and companies shedding space as leases expire.

Even there, there are a lot of buildings which have never come back close to the occupancy they regularly had pre-COVID.

"Starwood Capital Group is in default on a $212.5 million mortgage backed by an Atlanta office tower, another sign of mounting distress in US commercial real estate."https://t.co/KmaVOblufq

— John Wake (@JohnWake) July 20, 2023

When you have that sort of investment in a structure, you can’t afford to let it sit half empty, and the major firms aren’t waiting for the turn-around. They’re turning properties right back to the banks.

Barry Sternlicht’s Starwood Capital Group is in default on a $212.5 million mortgage backed by an Atlanta office tower, another sign of mounting distress in US commercial real estate.

The mortgage on Tower Place 100, in the Georgia capital’s Buckhead district, matured on July 9 and Starwood failed to refinance or pay off the debt, according to a filing compiled by Computershare.

…Corporate landlords, including Blackstone Inc. and Brookfield Asset Management Ltd., have stopped making payments on office buildings they’ve deemed to be money-losers as vacancies increased with the growing acceptance of remote work. In addition, borrowers’ financing costs have soared as the Federal Reserve hiked interest rates to cool inflation and property values have declined.

…Tower Place 100 was 62% leased as of the end of 2022, down from 87% in 2018 when the loan was originated. Among the 29-story building’s biggest tenants is WeWork Inc., the office-sharing company co-founded by Adam Neumann that has struggled financially.

The Atlanta area’s office-vacancy rate climbed to 22.4% in the second quarter, compared with the US average of 20.6%, according to brokerage Jones Lang LaSalle Inc.

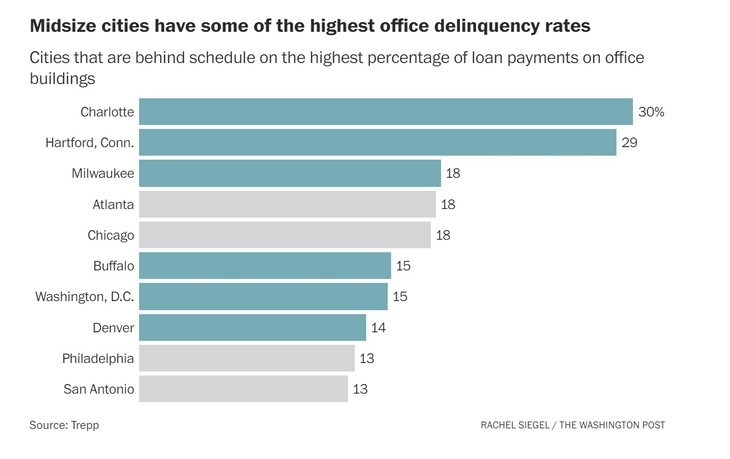

The WaPo says mid-size cities are having the worst experience with vacancy rates.

…All across the country, downtowns, office spaces and shopping centers are at risk of becoming ground zero for a new economic hazard: the urban doom loop. The fear is that a commercial real estate apocalypse could spiral out and slow commerce, wrecking local tax revenue in the process. Ever since the pandemic drove a boom in remote work, hubs such as New York and San Francisco have drawn attention for their empty offices in previously bustling skyscrapers. But many economists are even more worried about midsize cities that have fewer ways to offset the blow when a major company slashes office space, the sale price of a building craters, or a downtown turns into a ghost town.

The worst-case scenario would go like this: With more people working from home, companies from Milwaukee to Memphis are rethinking their leases or pulling out of them altogether. That drives vacancy rates up and makes it harder for landlords to attract new tenants or sell buildings for a healthy price.

Then property owners might struggle to pay off their mortgages or clear other debt. Business districts would dry up, stifling tax revenue from commercial properties or employee wages. Shoppers and tourists would have fewer reasons to venture downtown to eat or shop, choking off spending and forcing layoffs at restaurants and retail stores.

A CNBC commercial real estate investor who was being interviewed last week had no encouraging words for anyone involved in commercial real estate. He said “winter was coming” and it was going to be “very challenging for a long, long time.”

That has to curdle the stomach of even the most bullish of city officials.

This fellow said there are up to 40% of the offices vacant in Boston – BOSTON! – at any given time.

Kevin O'Leary reveals up to 40% vacancies of commercial buildings in Boston. A real estate crash would impact banks. pic.twitter.com/GJFdDdiALJ

— wakeup觉醒 (@wakeupusa777) September 17, 2023

Adding to the Bean Town building owners’ woes are announcements like these from local employers:

Boston’s biggest employers say five-day office weeks are over

Companies embrace flex schedules to accommodate workersThe five-day office work week may have gone the way of the Boston Braves.

Indeed, Beantown’s largest employers are having a hard time getting employees back to the office five days a week, as flexible work schedules and hybrid work arrangements have become the norm, the Boston Globe reported.

“I think most companies have resigned themselves to the fact that flexible work schedules are here to stay,” Jim Rooney, president of the Greater Boston Chamber of Commerce, told the outlet. “Could I see a day when it’s viewed as better for the business, better for the employee, and better for society if people are getting up and going to work? Yeah, I can see that coming back — but it’s not going to happen in the short term.”

…The report comes at a time when office values in Boston are cratering.

Real estate firm Synergy Investments recently purchased One Liberty Square, a 13-story office building in the Financial District of downtown Boston, for $45 million, which is a 17 percent decrease from the building’s value a decade ago, the Boston Globe reported.

“Cratering” is a bad word. It can be used to describe Atlanta’s business travel. No one is coming into the city anymore and not only are the hotels feeling it, all the convention related businesses are as well.

…Atlanta business travel is declining because one of its main drivers is visits made to customers or colleagues in their offices.

“If that person is not in that office, why would you still go to that city?” asked Jan Freitag, CoStar’s national director for hospitality analytics. “If you’re in your kitchen, let’s do that on Zoom.”

Some hotel owners are giving up. Arden Group defaulted last year on its $98.2 million mortgage on the Sheraton Atlanta, a convention-oriented property. This year, Ashford Hospitality Trust is handing back the keys to its lender on a portfolio of hotels including the W Atlanta, a luxury hotel near Peachtree Center.

Another reason for reluctance to force people to return downtown? Atlanta’s God awful traffic.

There’s no easy fix for any of that.

It’s looking like a perfect storm of bad news.

Join the conversation as a VIP Member