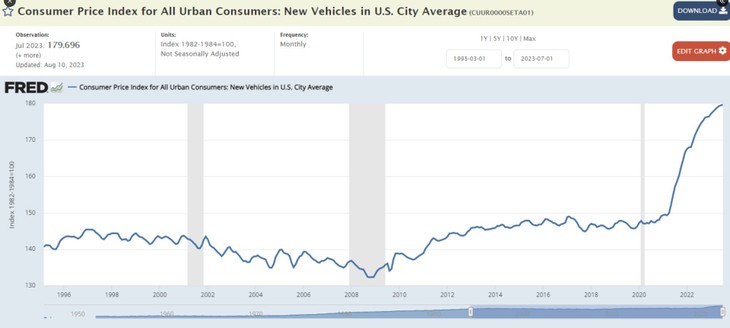

What in the wide, wide world of sports is going on with car prices? Now, I knew they were expensive – and we’ve already established how cheap I am – but, you know? It’s one of those things that doesn’t really smack you in the chops until you see a graph.

GULP

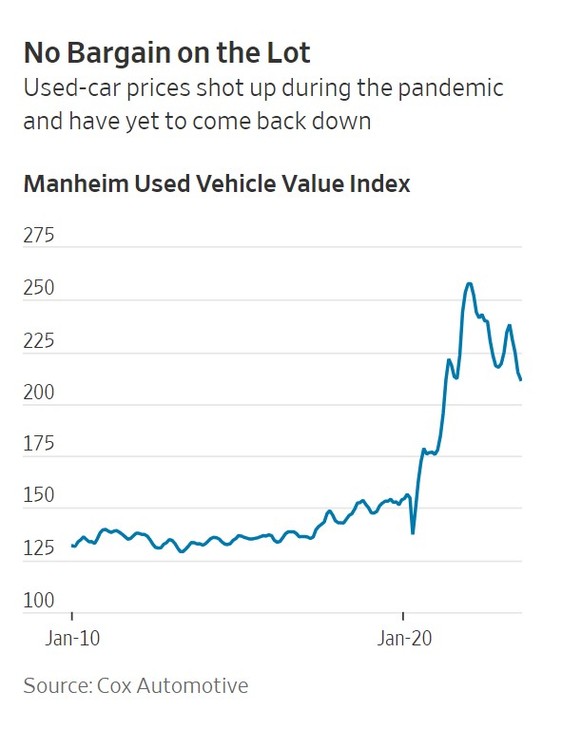

It’s not really any better with used cars, either. Gone are the days when you could find a reliable beater for $1500-2500 to get to work and back, or have the 17 year old “pay off” as he worked a part time job. My first car was 500 hard earned grocery store clerk bucks – ’67 Fairlane. Built like a tank and just what I needed as a 16 year old.

And all this before the UAW tries to stick a fork in the domestic automakers.

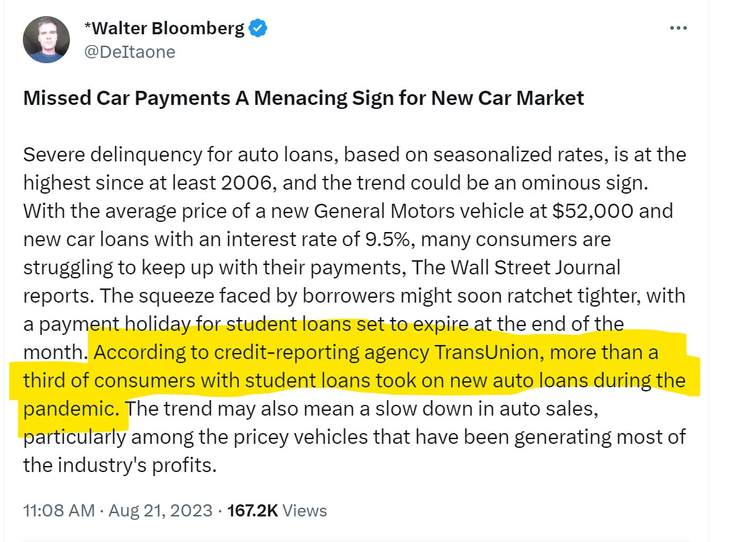

Interest rates are not helping the situation in the least. When an average car costs (GM says $52K) a quarter of what a nice house in the burbs did just a couple years ago, things are seriously out of whack. And when you have to have more down to get the loan because your credit is okay or you’re already overextended, and then it’s more a month to pay on it, welp. That’s a squeeze.

Cox Automotive figures it takes 42 weeks of income to pay off a new car.

Five years ago, there were a dozen models of new cars that sold for less than $20,000. In 2023, there was only one: the spartan Mitsubishi Mirage hatchback, which accounted for about 5,300 of the 7.7 million new vehicles sold in the U.S. in the first half of the year.

…Bargains have been hard to come by on the used-car lot as well, where the average vehicle listed for about $27,000—up more than 30% from prepandemic levels, according to Cox’s data.

Higher interest rates have made the situation more difficult for buyers. Today’s average new car loan has a monthly payment north of $750, with an interest rate of 9.5%. For used cars, the average rate is above 13.7%, according to Cox. The average term for loans issued over the past three years is nearly six years, according to data from Experian.

In 2019, the average monthly new car payment in America was $520.

Today over $725 (+39%)#bidenomics. pic.twitter.com/rCTTiMPAwr— Frog Capital (@FrogNews) August 21, 2023

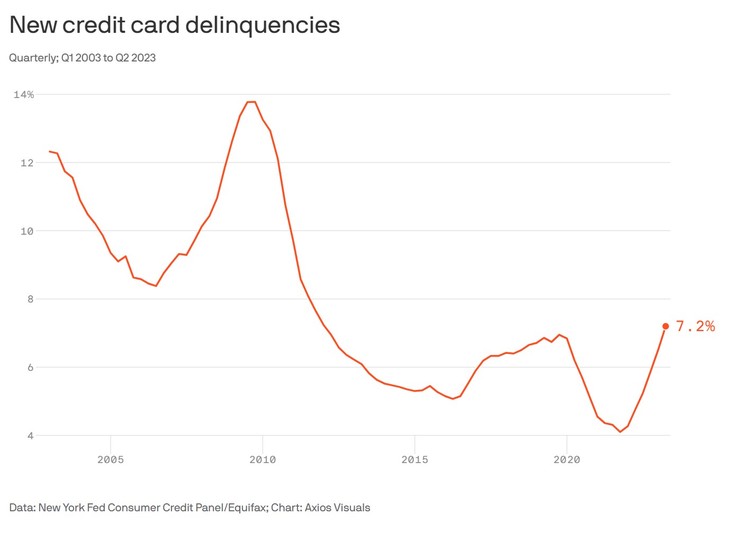

Delinquencies are trending up, which they said is quite unusual with unemployment so low. But I don’t think they’ve ever had to track auto loan defaults with balances this stratospheric before, either. Nor were they looking at write-offs on loans when the length of the term was 6 years. Gads, that’s a long time vice the 3, maybe 4 tops that used to buy the average vehicle.

…These numbers could explain a mystery bedeviling auto lending. Seasonalized rates of severe delinquency for auto loans are the highest since at least 2006, but the jobs market is strong.

But credit card delinquencies are up, too. Sign of the times or just #Bidenomics ?

There’s another wrinkle in the mix possibly fixin’ to spike auto sales and drive the delinquency rates higher. Remember the student loans? They’re going to have to start paying them. If you’ll remember, one of the worries was that during all that “pause” time, people came to think of that “extra” money they weren’t paying on their loans as theirs.

Turns out, that was true. They even bought cars with it.

It’s interesting, the contrast.

Back out to the driveway to sweet talk the ’96 Camry.

Oh, Eleanor, you paid-for beauty…

Join the conversation as a VIP Member